Yesterday, the European Central Bank released a report titled “The international role of the euro.”

You’ll notice they didn’t capitalize the title, perhaps as a subtle nod to the diminishing importance of the euro internationally…

I’m not going to bore you with details about the euro, but within the report there are some interesting facts that align neatly with my ongoing thesis for gold.

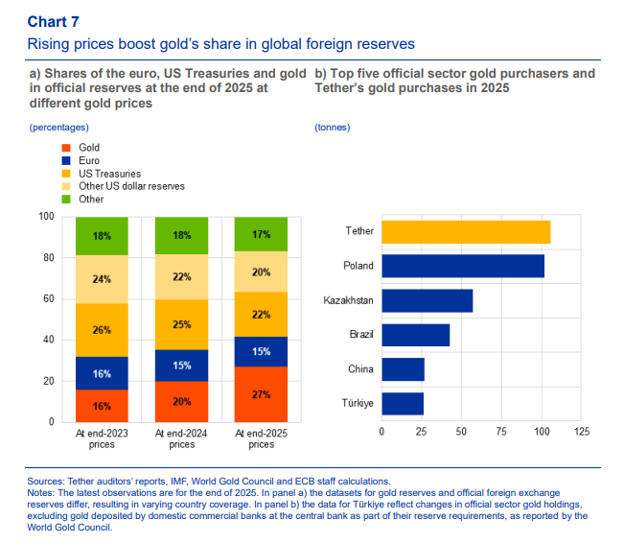

For one, faster than almost anyone could have predicted, gold overtook the dollar as the #1 reserve asset held by central banks.

Gold now makes up 27% of global reserves. You can see in the graphic above, the ECB decided to have gold represented by red, and the dollar represented by two different shades of gold. I present this observation without comment.

Also of note in the chart above: something I’ve been talking about for almost a year now, which is that Tether was the largest buyer of gold – outpacing (official) purchases from Poland, China, Turkey and Brazil.

Tether is buying something like 2 tonnes of gold per week, storing it in their own Swiss vaults and using it as a backstop for their crypto exchange, including Tether gold.

I expect that soon, Tether gold could be the main way that people own gold and even store their savings and transact with other people and businesses.

The big critique of gold forever has been that it’s inconvenient to use for daily purchases, and on the international scale, that it’s inconvenient and expensive to ship, store and transact in.

Tether gold solves this problem. It’s a tokenized stablecoin backed 1:1 with gold in Tether’s vaults that can be instantaneously and cheaply sent anywhere to anyone in tiny increments of 1/1000 of an ounce of gold.

That’s about $4.50 today.

Money flows to where it’s treated best. There’s no government currency out there that’s worth anyone’s trust. Tether gold is an escape valve for people all over the world to easily own gold instead of whatever local currency they’re forced to own and transact in today.

The ECB had to throw in this comment: “The share of gold now surpasses both that of the euro (15%) and US Treasuries (22%). However, this development largely reflects valuation effects.”

The problem with only noting the rise of gold’s price is that neither the ECB nor any other central bank ever seems to discuss the devaluation of the currencies they manage, nor how their purposeful devaluation plays out in the gold markets, which after all is priced in central bank-controlled currencies.

Over time, gold does a remarkable job of simply mirroring the increasing supply of dollars, euros, etc. – rising in price commensurate with the expansion of money supply.

Gold’s position as the top player in global reserves isn’t just the result of a “valuation effect” – it’s a direct consequence of purposeful, decades-long policy choices made by the ECB and other central banks.

The ECB claiming that gold’s emergence as the favored global reserve asset is the result of the price going up is a bit backwards:

The price is going up because the ECB and other central banks are willfully destroying their currencies to the point that even the banks have capitulated and bought record amounts of gold. They’re buying gold with THEIR currencies!

In the next page, the ECB seems to backtrack a bit, saying:

“However, gold purchases may also reflect efforts by some central banks to strengthen balance sheet resilience amid rising geopolitical risks. Survey data suggest that central banks hold gold not only for diversification but also as a hedge against geopolitical risk.”

There you have it: a ringing endorsement from the ECB to own gold.

Best,

Garrett Goggin, CFA, CMT

Lead Analyst and Founder, Golden Portfolio