No one in the mainstream media really talks about the Federal Reserve that much – outside of headline commentary about rate changes, you get zero analysis about the Fed.

That’s largely because no one outside of economists, bankers and sophisticated investors really knows much about the Fed and what it does.

Most of the time, it doesn’t matter. In a healthy, normal market, the Fed shouldn’t do much.

But over the past 40+ years, the Fed has been forced (or chose) to intervene in markets increasingly and with novel and far reaching policy in an effort to guide the economy in the direction that best serves U.S. monetary interests.

The Fed tells us they have a dual mandate of maximizing employment and keeping inflation at 2%. That’s what they say, anyway. But it doesn’t take a PhD in Central Bankspeak to know that at the margins, these two goals are in conflict. In short, the Fed sometimes has to choose between these goals – and sometimes it even has to favor other goals that are unstated – like the solvency of the Treasury market or defending the dollar system from foreign central banks.

Importantly, you don’t need to know how the inner plumbing of the Fed works to see what’s coming. The U.S. has the largest debt in world history and even the most rosy of projections shows this debt rising for the foreseeable future.

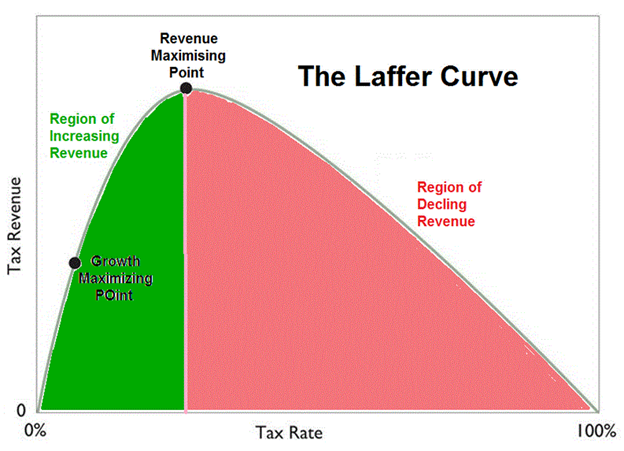

The paths to deal with this debt are all blocked. Raising taxes? Already mathematically an impossible solution. The Laffer curve shows tax receipts do not linearly increase with higher taxes.

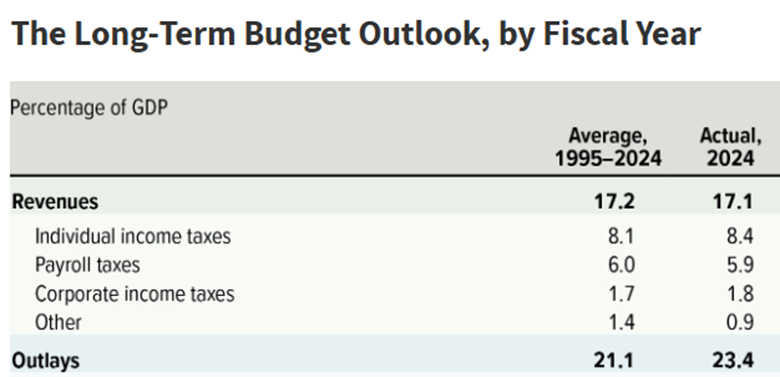

The U.S. has only ever been able to collect 17%-19% of GDP regardless of tax policy. High marginal rates, low marginal rates, high corporate tax, low corporate tax… tax receipts as a share of GDP never seem to break 20%.

Spending is already over 20% of GDP – meaning even if we could consistently tax 20% of GDP, we’d still be in the hole due to servicing the existing $38 trillion in existing debt.

It’s not going to happen with taxes.

Cutting spending?

Elon Musk and DOGE tried and even among the discretionary spending they targeted, it was both not enough and of course met with massive opposition. Cutting spending – real spending, on core unfunded liabilities like Social Security, Medicare – is off the table.

There’s been only one likely outlet to deal with debts: inflation. Inflation has the benefit of being nearly indistinguishable from growth when it comes to the same headline readers in the mainstream media who don’t know the difference between the Fed and the Treasury.

Authorities can then say we’re growing our way out of debt by pointing out GDP growth wrought by aggressive monetary policy that’s really just inflation.

President Trump has long been accused of simply saying out loud what most politicians only say behind closed doors, or perhaps never say at all.

Ever since Trump’s inauguration he’s been a very public advocate for aggressive rate cuts. He’s criticized Fed Chair Jerome Powell mercilessly for not cutting rates fast or far enough.

Trump will soon nominate a new Fed Chair who appears to be much more dovish than Powell.

The goal: blow out all the stops to juice inflation (or “growth” if you prefer), which will boost asset prices across the board. If the timing is right, this monetary revolution will have the appearance of helping everyone feel more prosperous heading into next year’s mid-terms.

The unspoken role and policy of the Fed has been very simply to help kick the debt can down the road while not blowing up the economy completely.

That’s it.

That’s what Trump is going to facilitate.

Meanwhile, what do you suppose will happen to gold and gold stocks?

The market still hasn’t caught up to the value proposition of the best gold stocks at $3,000/oz gold, let alone $4,000/oz gold – or higher.

Just wait until Trump and his new money-printer Fed governor put the pedal to the floor.

I don’t think we’ve seen anything yet for this gold bull.

Best,

Garrett Goggin, CFA, CMTLead Analyst and Founder, Golden Portfolio