The best investment thesis requires constant upkeep, questioning, re-examining of the basic landscape.

For gold, the long-term story needs to be considered – even if it seems like a foregone conclusion.

Remember: most major financial crashes occur downstream of millions of people thinking “I can’t lose!”

That line of thinking typically comes after decades of relative safety and outperformance in an asset class. Think: Investment Trusts in the 1920s, Savings and Loan in the 1980s, real estate leading up to the Great Financial Crisis, etc.

Without a widespread public belief about safety and “guaranteed returns” these assets don’t ever get to bubble territory.

You don’t want to invest in a bubble near the top!

So, it’s worth going through the paces to make sure your current investment thesis for gold is still intact.

From my perspective, you have to be nimble in the short term, and know when to take profits (as I recommended in late December through late January) but you also need to look at the long-term trajectory.

So, I’ve put together a quick punch list of where my mind goes when I think through what’s going on for gold…

Where is gold in the bull trend?

It’s impossible to pinpoint exactly where we are in a bull trend, but we can look at historic examples.

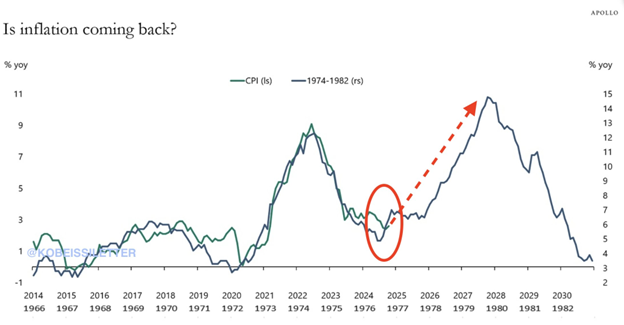

If you assume our current bull run started around 2020, it looks like we’re about halfway through, and it looks like we’re bouncing around on the same inflation trajectory too.

Part of gold’s appeal is as an inflation hedge. Those expectations can build up a lot of momentum for the price of gold if inflation ticks up…

What obstacles could stop or reverse the price of gold?

We’re currently experiencing one of the short-term catalysts for a correction in gold’s price. For one, you don’t typically have a correction to the downside if you haven’t recently seen a massive run on the upside.

But global war, a supply crunch on an important commodity like oil, and uncertainty and disruption in the market will tend to send gold lower over the short term.

As important as gold is in the global financial system, most assets are still settled in dollars (or other major currencies.)

So, gold gets sold when people need to raise cash. If the war worsens or the supply shock goes on for a long time, that might mean an even deeper correction for gold. It’s not something I’m particularly worried about because I think we would still be well above gold prices of a year ago, but it’s a distinct possibility to consider.

What competition does gold face as a monetary asset?

One of the major drivers of gold’s price is its function as a global monetary asset. The big knock on gold is that it pays no yield… But once you account for inflation, there really aren’t many (or any) global currencies that do pay a yield.

The dollar, euro, and other western currencies all fail that “positive real yield” test. It’s one of the main reasons we’ve seen central banks buying gold over the past 10 years.

Countries outside of America’s direct sphere of influence, like China, Russia, Brazil and India are all net buyers of gold. Far from trying to compete with gold, they’re adding it to their balance sheet.

Russia recently joined China in saying it will ban the export of gold. I’ve talked in the past about the BRICS currency that’s being rolled out called “the Unit” which is itself partially backed by gold.

What about Bitcoin and other cryptocurrencies? From my experience, people who are bullish on BTC are also typically bullish on gold. We’re also seeing some exciting developments with major cryptocurrency firms like Tether partnering with gold companies, buying lots of gold to backstop their stablecoins, etc.

There’s maybe some social media driven antagonism between goldbugs and BTC “hodlers” but I don’t view gold and BTC in competition with each other. They perform different functions – though I of course am partial to gold due to its 5,000 year history as a monetary asset.

How does the current average portfolio ownership of gold compare to previous periods?

According to a January 2026 article written by Wisdom Tree, most investors only hold between “0%-3%” in gold.

In other words, most investors have no gold position whatsoever. There is not a widespread interest let alone ownership of gold or gold stocks. Most people are extremely underweight these positions!

When we start to see the average investor holding 5% or more of their investments in gold, then we can start talking about being close to the end of the bull run…

But I firmly believe we’re not even close to that point yet.

Best,

Garrett Goggin, CFA, CMT

Lead Analyst and Founder, Golden Portfolio