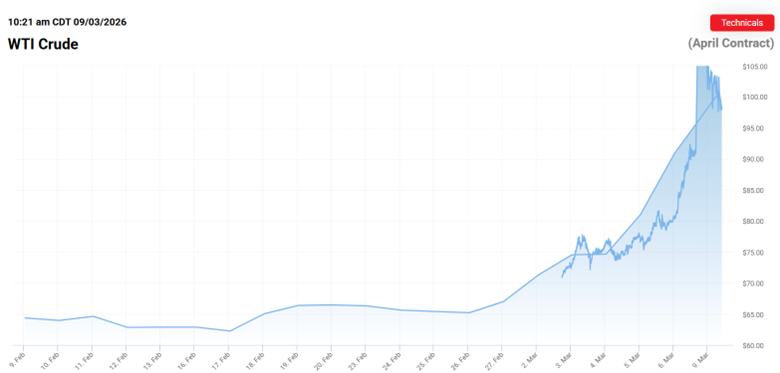

Since the beginning of this bull market in gold, the miners have enjoyed what can only be described as record low oil prices.

Adjusted for inflation, the $60-$70 oil we’ve seen over the past two years is cheaper than we saw for the entire 2000s and most of the 1980s – periods when the US underwent significant economic growth.

Cheap oil is a key part of profitable production for everything – but especially for gold.

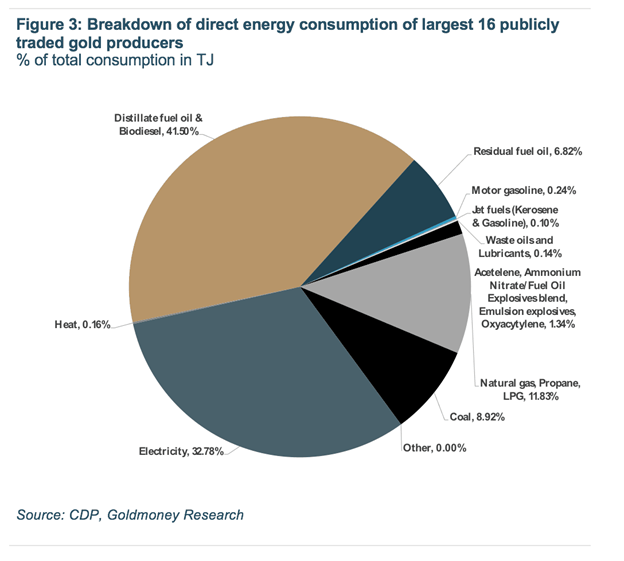

Oil is a major price input for the production of gold – and not just because all of the machinery, the trucks, the drill rigs, etc. that run on diesel, but because everything used in mining also requires oil to produce. The tires, explosives, lubricants, electricity, the machinery itself, all of the steel, all of the concrete, the buildings, the electrical components, etc.

It all has oil as a major part of the price component.

Estimates put oil costs as a 15-25% input of the all-in-sustaining-costs for producing every ounce of gold.

But if oil doubles in price, that range moves to 30%-50%…

Oil hasn’t quite doubled yet, but every dollar a gold miner has to pay for oil is a dollar that’s not hitting the bottom line of profitability.

This circumstance is exactly why most gold majors fail to remain profitable over the long term. Their costs tend to rise with inflation at about the same rate that inflation pushes gold prices higher.

It’s a near-impossible treadmill which is why you can count the number of long term highly profitable gold majors on one hand even if you’ve had a woodworking accident that’s taken most of your fingers.

Oil prices at over $100/barrel take a significant chunk of profitability out of every gold producer, right off the top.

That’s why I mostly focus on junior and midcap firms that are mostly pre-production.

These kinds of gold stocks have leverage to the gold in the ground, and we have a major advantage in evaluating these companies because most investors (including most of Wall Street) have zero clue how to analyze these pre-production firms.

Until the very tail end of the bull market, these kinds of firms will be wildly undervalued and even ignored.

We’re not there yet.

We still have dozens of high quality, early stage juniors and mid cap miners to pick from.

Higher oil prices may spook the market lower – which will only serve to make these opportunities better for the long term.

Don’t miss this chance to get into some excellent deals…

Best,

Garrett Goggin, CFA, CMT

Lead Analyst and Founder, Golden Portfolio