Gold stocks are cyclical. There are certain times when you have to own them, and now is one of those times. I’m a value investor, and I’ve rarely seen an opportunity like this in Gold stocks. The GDX is selling at nearly a 20% discount to fair value based on FCF/share. An occurrence that only happened twice over the past 10 years in 2015 and 2020. Both times resulted in the GDX rising at least 100% over the following 6 months. The rare signal has appeared again with the GDX now selling at 17% discount to fair value. Don’t let this opportunity pass you by.

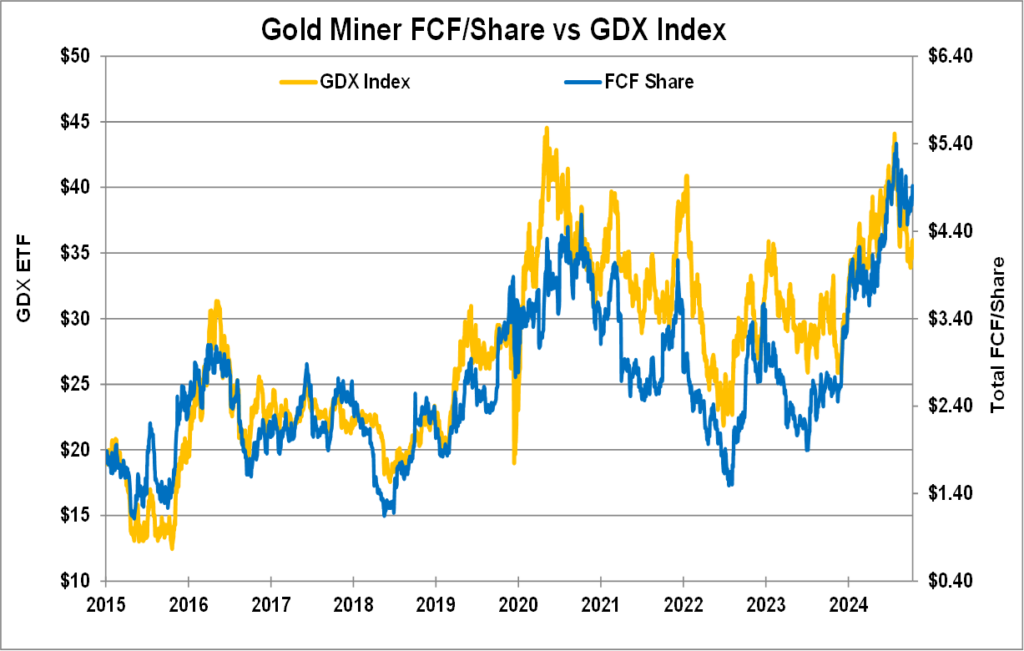

Take a look at the chart below of Free Cash Flow per share of the top 5 miners (Newmont, Barrick, Kinross, Anglo and Agnico) vs the GDX. Note the correlation is very high at 87%. All stocks represent the lifetime profits over the life of an asset, and Gold Miners are no different. You can see how the GDX ETF follows FCF/share of the Miners. The yellow line GDX trades above the blue line FCF/share the majority of time. But notice the gap between the yellow line GDX ETF that is now below the blue line FCF/share. That’s your valuation gap opportunity.

The top 5 Gold Miners last quarter’s annualized production was 21,188K ounces with an average AISC $1,503/oz. At current Gold price of $2,690/oz, the top 5 Miners are generating $25,143 mil FCF. With total 5,114 mil shares outstanding, is worth $4.92 FCF/share. Since the GDX is so highly correlated with FCF/share we can use a regression study to determine where the GDX should be trading at based on $4.92/share of FCF.

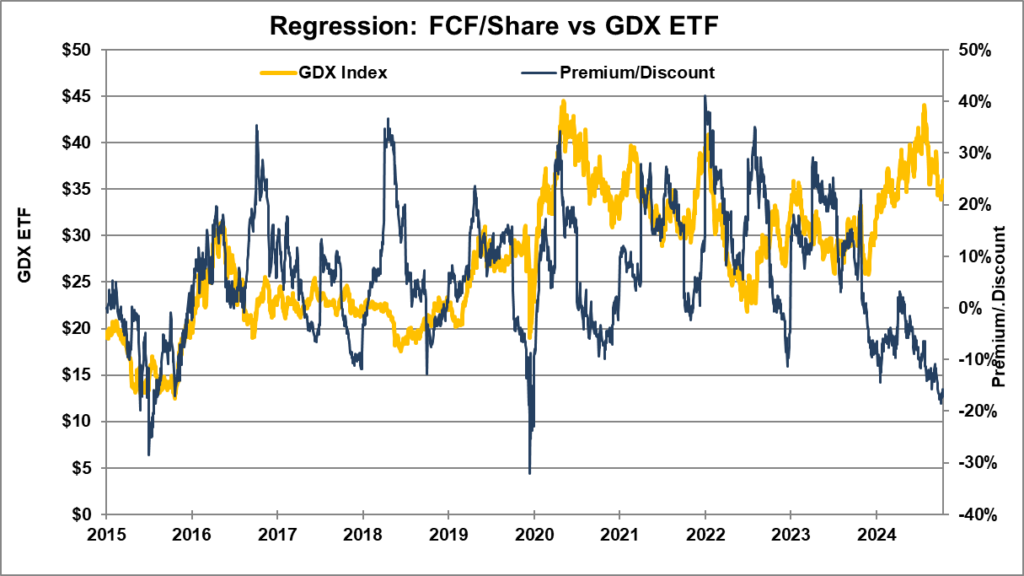

The study shows that the GDX should be trading at $42.55 per share with $4.92/share of FCF. The GDX is only trading for $35.35 per share which is nearly 20% lower than fair value. Large discounts like this don’t occur very often. GDX undervaluation based on FCF/share only reached 20% three times since 2015. Once, in 2015 when the Fed embarked on a rate hiking cycle. And latest was in 2020 when the Fed launched QE4 to deal with the Covid crisis. Both times in 2015, and 2020 Gold stocks and the GDX quickly doubled both times over the next few months. Now in 2025, the GDX is undervalued by 17% based on underlying FCF of $4.92/share.

I expects this undervaluation in 2025 to be resolved just like the last two times, with Fed action. Usually when the Fed eases bond yields fall. But this time is different. The Fed cut rates in 2024 from 5.5% to 4.5%, but the 10 year note keeps rising from 3.6% at 1st cut in September to 4.78% now. The Fed just had to back off the easing cycle due to a vibrant jobs report last week and inflation fears.

Trump has clearly stated he needs lower rates to drive his economic revival. Treasury Secretary Bessent has stated the need for a “Shadow Fed” member to integrate the Treasury with the Fed. Fed Vice Chair Michael Barr just stepped down from the Fed. Trump selection Michele Bowman is his projected replacement. Mrs. Bowman dissented against cutting rates last meeting, so she leans hawkish. But she seeks to dismantle Basel III which imposed strict capital controls on the banks, so she’s a pragmatist focused on economic growth.

I distinctly sees Yield Curve control to be implemented by the Fed. On the surface this would allow the Fed to remain vigilant against inflation by keeping its Fed Funds rate high. The Fed would be enabled to use its balance sheet to purchase massive amounts of long end Treasury debt helping to keep bond yields low. YCC is direct monetization of US debt and a massive step in the wrong direction. Gold will do what it always has acting as the monetary canary in the coal mine and climb higher.

Now is the perfect time to take advantage of the rare discount opportunity. If you’ve missed my latest briefing where I go into detail on how best to take advantage of this opportunity you can read it here.

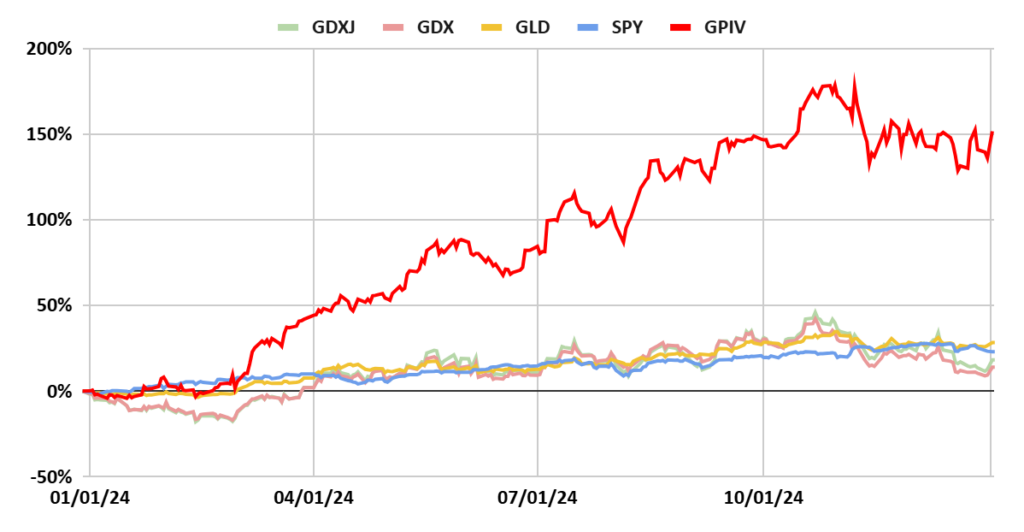

As many of you know, I’ve been a precious metals mining analyst for around 20 years, and I know where value is created in the Mining industry. My Golden Portfolio IV (GPIV) portfolio rose 136% in 2024 alone.

Who Makes The Cut?

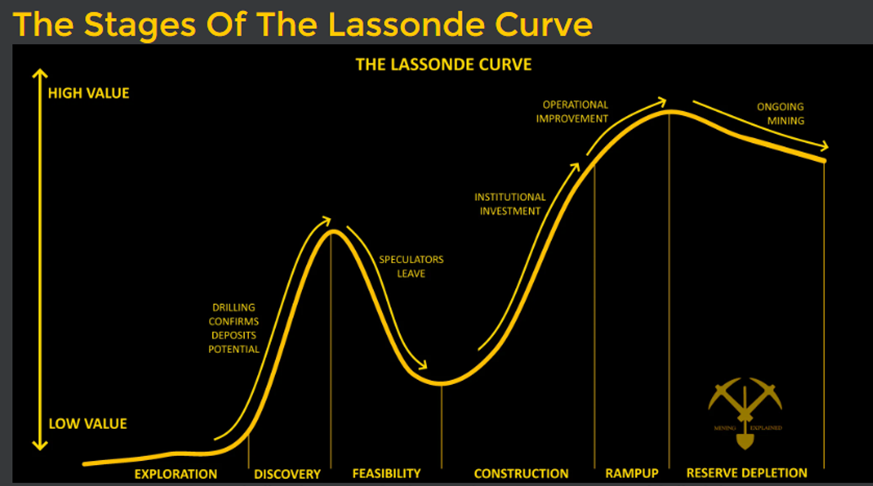

I find the explorers and developers in the troughs of the Lassonde curve. Not much value is awarded to explorers with a prospective property. Often time these claims represent a liability more than an asset. But once a high grade drill hole is reported the market begins to move the share price higher. It often takes years for an explorer to define the limits of the high grade mineralization, and prove out the deposit. Value is created every step of the way.

The second trough occurs after an economic study is published. The developer now has to finance building the project to bring the mine into production. Uncertainty is high. It’s possible equity holders could be diluted out of major gains from a poorly constructed capital raise.

When shareholder aligned management raises the funds needed correctly by protecting equity holders, the shares begin to rise anew. Some fully financed developers in the GPIV still trade for up to 80% discount to fair value. To get access to these companies and my full company analysis on them click here. It’s a two to three year window during construction where market value rises to meet lifetime FCF. When a project is fully built, and ready to start production, Gold price uncertainty is eliminated, enabling the Developer to trade at full valuation.

I know how to find the miners that can rise in value regardless of whether the Gold price increases or declines. Explorers and Developers in the troughs of the Lassonde curve simply need to execute. Explorers need to drill and prove out their resource. Developers need to build out their projects enabling them to convert ore to Gold and profits. GPIV companies are so undervalued that even if the Gold price falls, they still have the opportunity to drive value through execution, de-risking the company which will push the share price higher.

Even after rising 136% in 2024 GPIV Companies are still trading at massive discounts to fair value ranging from 55% to 96% based on a $2,700/oz Gold price. GPIV holdings still need to rise another 2X to 25X to meet fair value. It looks like another strong year for Gold is upon us. GPIV members should rise, driven by execution and increased lifetime FCF project value based on a rising underlying Gold price.

Best,

Garrett Goggin, CFA